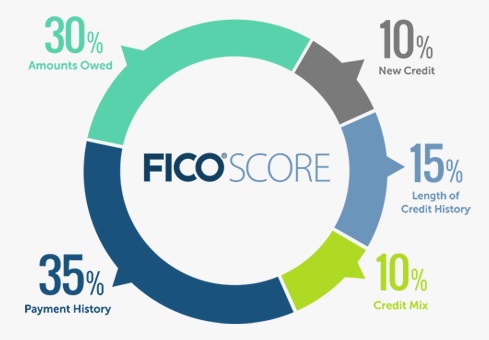

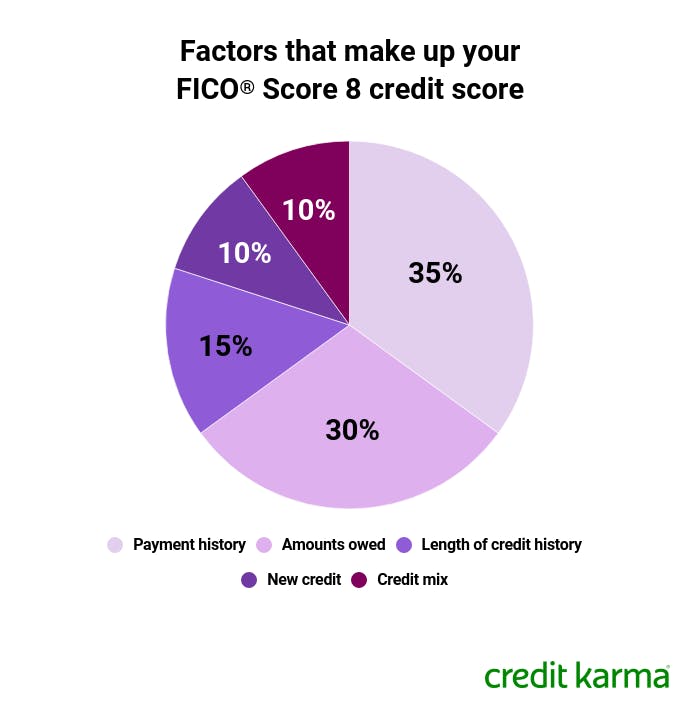

Carrying too much credit card debt can lead to a lower credit score. Credit utilization is a measure of how much credit you use compared to your total credit line. Keeping your balances on your cards at 20% or less of their maximum limits will help raise your credit score.

Credit card debts can be paid off to lower your credit score

Although paying off your credit card debt is a good way to reduce your debt, it can also affect your credit score. This is due the effect credit card debt has on your credit utilization, or how much credit you have used. Ideal credit utilization should be between 10% and 30 percent. It's important to remember that a decrease in your credit score is temporary. Your credit score can improve over time by allowing for a few months.

Paying off your credit cards debt will not only lower your score temporarily but also have positive consequences for your financial health. You can end up paying more monthly for interest and late fees if your credit card balance is not paid off. Credit utilization is an important factor in your credit score. High credit utilization will affect your credit score.

Missing payments can bring down your credit score

The frequency with which you pay your bills is one of the main factors that can affect your credit score. Several missed payments can knock up to 100 points off your total score. You can reduce the impact on your score if you make regular payments. For instance, if your credit card bills are paid on time and other payments are not delayed, you won't lose any points.

While the repercussions of missing a payment may be harsh, they can be overcome with time, hard work, and patience. Making the minimum payment on schedule can help you start a new streak. Additionally, it is possible to work towards reducing your debts by actively paying off past debts.

Multiple credit card applications can lower credit scores

Multiple credit card applications at once can have a compounding effect that can lead to lower credit scores. Lenders may be concerned about multiple applications. They will consider it a sign that you are in financial distress. Your score can be restored by making spaced out applications and using responsible credit responsibly. You can also benefit from rewards programs by having multiple credit cards.

When applying to multiple credit cards, it is important to know your utilization ratio. Your utilization ratio represents the percentage of available credit you are currently using. Your overall utilization should not exceed 30%. Although having multiple cards with a low usage rate will lower your overall utilization percentage, it is important not to exceed 30%. Credit score reductions will occur if your credit utilization rate is greater than 30%.

Your credit score will be raised by keeping your credit card balances below 20% of the maximum limit

Experts recommend that credit card debts are kept below 20% of the limit. This will keep your credit utilization low, which will help boost your credit score. However, it is important to note that credit utilization is not the only factor that affects your score. Your score can be affected by late payments or other credit-related issues.

Credit cards are more convenient than cash, and they are accepted in many places. They are more secure than cash and offer several benefits. You can cancel the account at any time if your credit card is stolen or lost. The card owner will often receive reimbursement if the card is returned. If you pay the balance in full each month, interest can be avoided. Many credit cards offer a one-year interest-free period for purchases. However, it is important to learn when the interest-free period ends and what spending will not count.

FAQ

When should you start investing?

On average, $2,000 is spent annually on retirement savings. However, if you start saving early, you'll have enough money for a comfortable retirement. If you wait to start, you may not be able to save enough for your retirement.

You must save as much while you work, and continue saving when you stop working.

The sooner you start, you will achieve your goals quicker.

Consider putting aside 10% from every bonus or paycheck when you start saving. You may also invest in employer-based plans like 401(k)s.

Make sure to contribute at least enough to cover your current expenses. After that, you will be able to increase your contribution.

How can I reduce my risk?

Risk management means being aware of the potential losses associated with investing.

One example is a company going bankrupt that could lead to a plunge in its stock price.

Or, a country could experience economic collapse that causes its currency to drop in value.

You risk losing your entire investment in stocks

It is important to remember that stocks are more risky than bonds.

You can reduce your risk by purchasing both stocks and bonds.

By doing so, you increase the chances of making money from both assets.

Another way to minimize risk is to diversify your investments among several asset classes.

Each class has its unique set of rewards and risks.

For instance, stocks are considered to be risky, but bonds are considered safe.

You might also consider investing in growth businesses if you are looking to build wealth through stocks.

Saving for retirement is possible if your primary goal is to invest in income-producing assets like bonds.

Which type of investment yields the greatest return?

It is not as simple as you think. It all depends on how risky you are willing to take. If you put $1000 down today and anticipate a 10% annual return, you'd have $1100 in one year. If you instead invested $100,000 today and expected a 20% annual rate of return (which is very risky), you would have $200,000 after five years.

The return on investment is generally higher than the risk.

The safest investment is to make low-risk investments such CDs or bank accounts.

This will most likely lead to lower returns.

Conversely, high-risk investment can result in large gains.

For example, investing all of your savings into stocks could potentially lead to a 100% gain. But it could also mean losing everything if stocks crash.

Which is the best?

It all depends what your goals are.

To put it another way, if you're planning on retiring in 30 years, and you have to save for retirement, you should start saving money now.

However, if you are looking to accumulate wealth over time, high-risk investments might be more beneficial as they will help you achieve your long-term goals quicker.

Remember: Riskier investments usually mean greater potential rewards.

But there's no guarantee that you'll be able to achieve those rewards.

Which investments should a beginner make?

Investors new to investing should begin by investing in themselves. They should also learn how to effectively manage money. Learn how to save money for retirement. How to budget. Find out how to research stocks. Learn how financial statements can be read. Learn how to avoid scams. Learn how to make sound decisions. Learn how diversifying is possible. Learn how to protect against inflation. Learn how to live within ones means. Learn how wisely to invest. You can have fun doing this. You will be amazed by what you can accomplish if you are in control of your finances.

Should I diversify the portfolio?

Diversification is a key ingredient to investing success, according to many people.

In fact, financial advisors will often tell you to spread your risk between different asset classes so that no one security falls too far.

This approach is not always successful. It's possible to lose even more money by spreading your wagers around.

For example, imagine you have $10,000 invested in three different asset classes: one in stocks, another in commodities, and the last in bonds.

Let's say that the market plummets sharply, and each asset loses 50%.

You have $3,500 total remaining. However, if you kept everything together, you'd only have $1750.

So, in reality, you could lose twice as much money as if you had just put all your eggs into one basket!

It is essential to keep things simple. Take on no more risk than you can manage.

How do you start investing and growing your money?

You should begin by learning how to invest wisely. This will help you avoid losing all your hard earned savings.

You can also learn how to grow food yourself. It's not nearly as hard as it might seem. With the right tools, you can easily grow enough vegetables for yourself and your family.

You don't need much space either. However, you will need plenty of sunshine. Also, try planting flowers around your house. They are very easy to care for, and they add beauty to any home.

You might also consider buying second-hand items, rather than brand new, if your goal is to save money. They are often cheaper and last longer than new goods.

Statistics

- Over time, the index has returned about 10 percent annually. (bankrate.com)

- An important note to remember is that a bond may only net you a 3% return on your money over multiple years. (ruleoneinvesting.com)

- As a general rule of thumb, you want to aim to invest a total of 10% to 15% of your income each year for retirement — your employer match counts toward that goal. (nerdwallet.com)

- According to the Federal Reserve of St. Louis, only about half of millennials (those born from 1981-1996) are invested in the stock market. (schwab.com)

External Links

How To

How to Save Money Properly To Retire Early

Retirement planning involves planning your finances in order to be able to live comfortably after the end of your working life. It's the process of planning how much money you want saved for retirement at age 65. You also need to think about how much you'd like to spend when you retire. This includes travel, hobbies, as well as health care costs.

You don’t have to do it all yourself. Financial experts can help you determine the best savings strategy for you. They'll look at your current situation, goals, and any unique circumstances that may affect your ability to reach those goals.

There are two main types, traditional and Roth, of retirement plans. Traditional retirement plans use pre-tax dollars, while Roth plans let you set aside post-tax dollars. It all depends on your preference for higher taxes now, or lower taxes in the future.

Traditional Retirement Plans

Traditional IRAs allow you to contribute pretax income. If you're younger than 50, you can make contributions until 59 1/2 years old. You can withdraw funds after that if you wish to continue contributing. After turning 70 1/2, the account is closed to you.

If you already have started saving, you may be eligible to receive a pension. These pensions vary depending on where you work. Some employers offer matching programs that match employee contributions dollar for dollar. Some offer defined benefits plans that guarantee monthly payments.

Roth Retirement Plans

Roth IRAs do not require you to pay taxes prior to putting money in. You then withdraw earnings tax-free once you reach retirement age. However, there are some limitations. For medical expenses, you can not take withdrawals.

Another type of retirement plan is called a 401(k) plan. These benefits may be available through payroll deductions. Extra benefits for employees include employer match programs and payroll deductions.

401(k), plans

401(k) plans are offered by most employers. With them, you put money into an account that's managed by your company. Your employer will automatically contribute a percentage of each paycheck.

You can choose how your money gets distributed at retirement. Your money grows over time. Many people want to cash out their entire account at once. Others may spread their distributions over their life.

You can also open other savings accounts

Some companies offer other types of savings accounts. TD Ameritrade has a ShareBuilder Account. This account allows you to invest in stocks, ETFs and mutual funds. Plus, you can earn interest on all balances.

Ally Bank offers a MySavings Account. This account can be used to deposit cash or checks, as well debit cards, credit cards, and debit cards. You can then transfer money between accounts and add money from other sources.

What's Next

Once you have a clear idea of which type is most suitable for you, it's now time to invest! Find a reliable investment firm first. Ask your family and friends to share their experiences with them. Also, check online reviews for information on companies.

Next, you need to decide how much you should be saving. This step involves figuring out your net worth. Net worth can include assets such as your home, investments, retirement accounts, and other assets. It also includes liabilities like debts owed to lenders.

Once you know your net worth, divide it by 25. This number will show you how much money you have to save each month for your goal.

You will need $4,000 to retire when your net worth is $100,000.